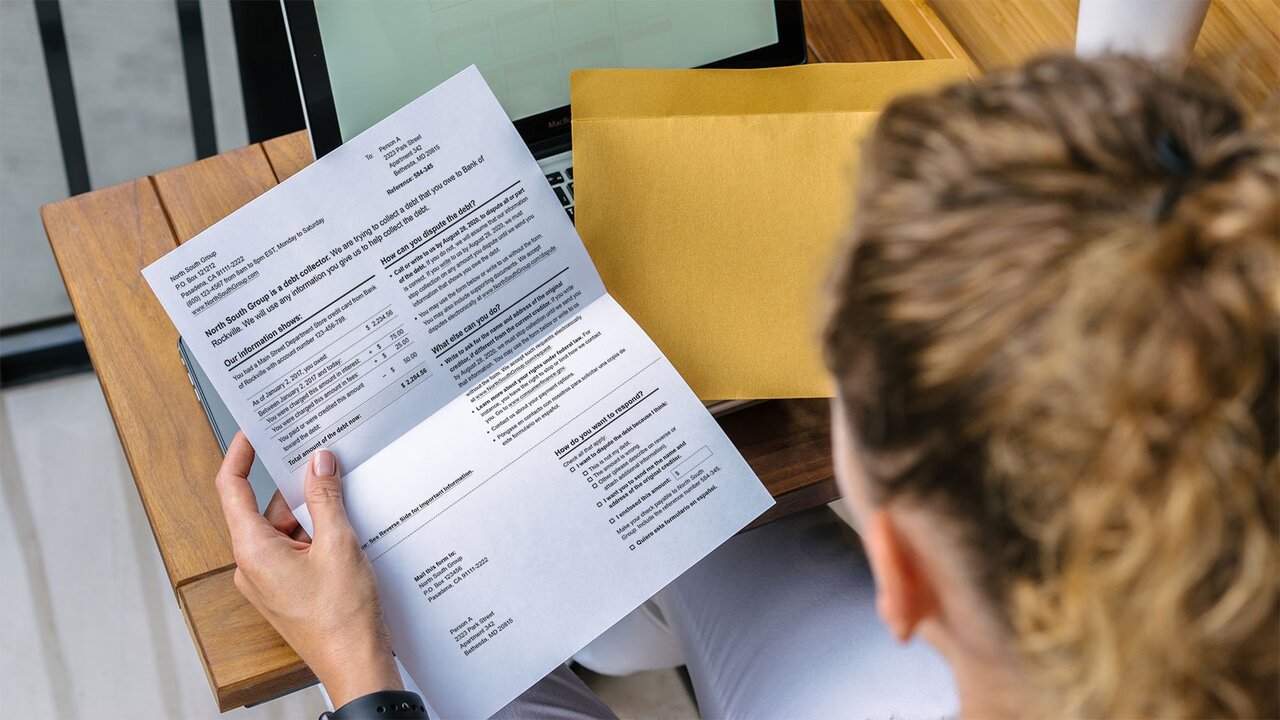

Receiving a call from a debt collector can be stressful and intimidating. But debt collection in Canada is a heavily regulated industry, and there are strict rules about what collectors can and cannot do. Knowing your rights is the first step to protecting yourself.

How Debt Collection Works in Canada

When you owe money and miss payments, the original creditor — such as a credit card company, phone provider, or bank — may attempt to collect the debt themselves. If they are unsuccessful, they may hire a third-party collection agency or sell the debt to one. Both individual collectors and collection agencies must follow provincial regulations in the jurisdictions where they operate.

Rules About Contacting You

When They Can Call

Debt collectors are generally restricted to calling between 7 a.m. and 10 p.m. on weekdays, with more limited hours on weekends. In Quebec and British Columbia, the initial contact must be in writing — not by phone. In Quebec, no contact is permitted on Sundays or statutory holidays.

How Often They Can Call

In Ontario, once a collector has made initial contact, they are limited to calling or writing no more than three times per week. This limit includes voicemails and emails.

Contacting Your Employer or Family

Collectors can contact your employer, friends, or family only under limited circumstances — generally to obtain your address or phone number, or to reach a guarantor. In most cases, they need your written permission to contact people you know.

Communicating Through Your Lawyer

In some provinces, if you provide a written request directing the collector to communicate through your lawyer — along with your lawyer's contact information — they must comply.

What Collectors Cannot Do

Debt collectors are prohibited from:

Secured vs. Unsecured Debt

It is important to understand the type of debt you owe. Secured debts — like mortgages and car loans — are backed by an asset. If you default, the creditor may have the right to seize the asset with less formality. Unsecured debts — like credit cards and gym memberships — do not have collateral behind them, which means the collection process is different.

Protect Yourself

Before responding to any debt collector, review your original agreement and the latest invoice to confirm the amount owed. Check whether the limitation period for legal action on the debt has passed — in Ontario, for example, a debt older than two years generally cannot result in a lawsuit.

How a Personal Legal Service Plan Can Help

A Personal Legal Service Plan gives you access to a dedicated Provider Law Firm in your province or state with experienced consumer protection and debt Lawyers who can review your debt situation, explain your rights under provincial law, communicate with collectors on your behalf, and help you take control of the process.

Ready to Get Protected?

Get affordable legal protection today. Choose your location to explore Personal Legal Service Plans.